Nov 18, 2025

Other Posts

What are DATs?

Digital Asset Treasuries (DATs) are publicly traded companies that make on-chain assets (such as BTC, ETH, SOL) a core part of their balance sheet and strategy, giving investors equity exposure to those assets plus whatever operating leverage and additional benefits the team can add.

In practice, DATs raise capital via equity offerings, convertible notes, or debt, and deploying it into crypto. Many of them can or have plans to further expand the treasury’s utility by putting it to work by staking PoS assets, using liquid staking tokens, lending, or collateralized borrowing to generate yield and grow holdings. Unlike ETFs, DATs can time purchases, use financing, and actively manage exposure, which can expand Net Asset Value (NAV) per share over time.

For investors, returns can come from three places: the underlying token appreciation, treasury growth per share (via accumulation and yield), and the equity premium/discount the market assigns to the share. This mix is what differentiates DATs from simply holding crypto or buying an ETF.

What’s Driving the Rise of DATs Today?

With the appearance of dozens of Digital Asset Treasuries (DATs), it’s clear that this is a new class of vehicle for retail to enter crypto, and it is well different from traditional treasuries built around cash and bonds. The model isn’t at an experiment-stage anymore either: early movers like MicroStrategy have already proved the model with large, sustained BTC accumulation, and a newer wave is expanding beyond Bitcoin into ETH and SOL, effectively treating crypto assets as core balance sheet reserves rather than merely risky bets.

What sets DATs apart is that they’re not just passive wrappers. They can raise capital (equity, debt, etc.), deploy it into crypto, and then work those reserves through staking, lending, collateralized borrowing, or even restaking, to grow holdings and NAV per share over time. That means shareholders can capture both market appreciation and treasury expansion, which are benefits that users don’t get from holding ETFs, for example.

So why are DATs going all-in now? A mix of factors: ETFs as on-ramps bringing regulated capital into BTC/ETH, a more favorable regulatory landscape, a favorable rate scenario that’s changing how investors view cash vs. scarcity assets, compounding treasury growth potential that accrues NAV per share, and the possibility for deeper DeFi integration that can turn static reserve balances into productive capital. Let’s break down each factor.

ETFs as On-Ramps

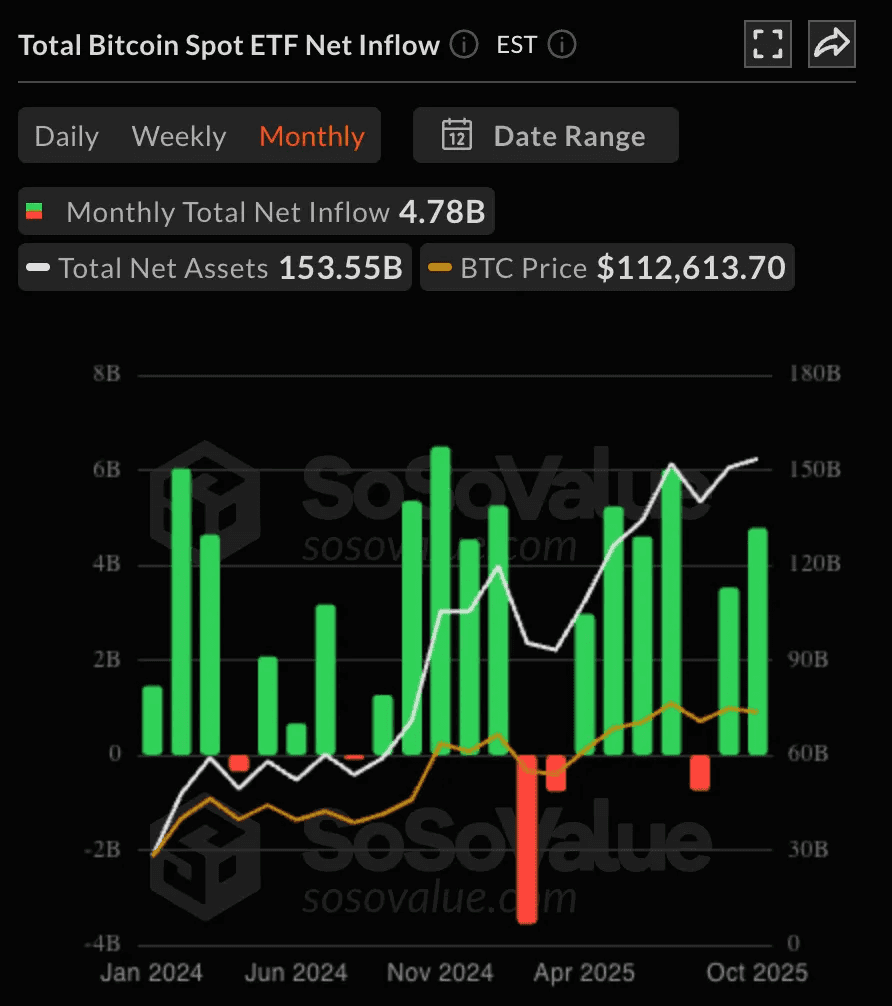

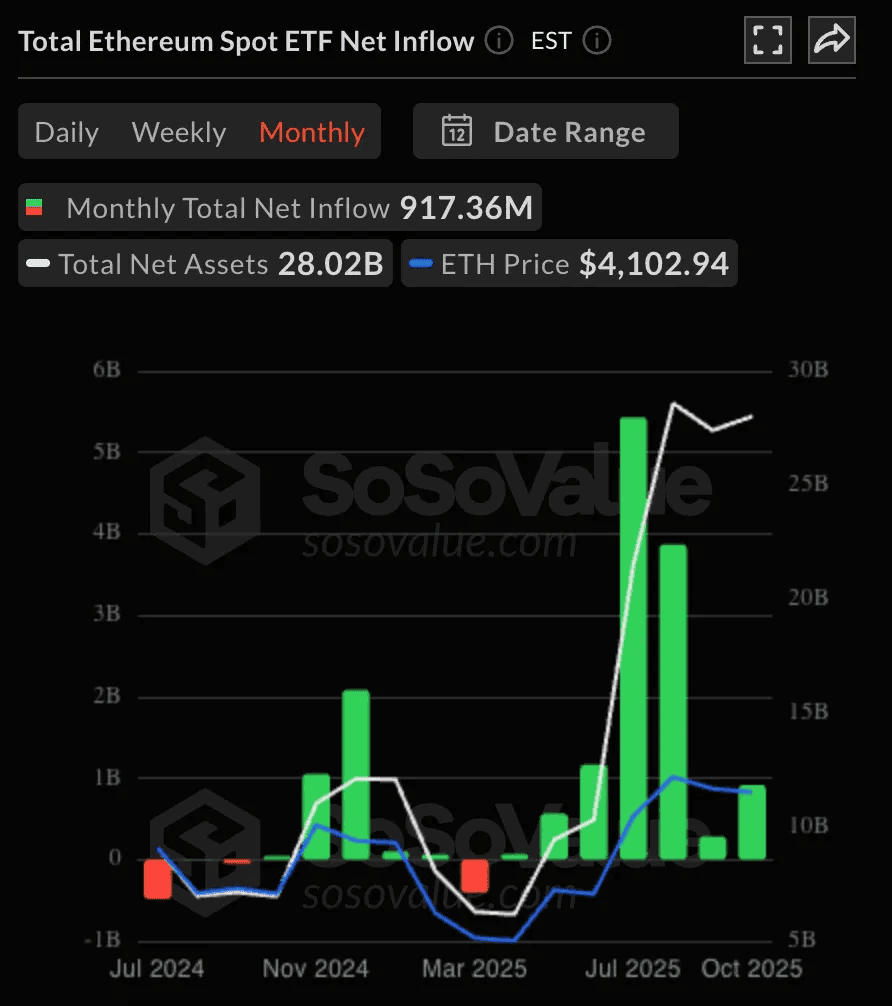

Since the approval of spot BTC ETFs back in 2024, demand has been staggering: daily trading volume surpasses $7B, and BlackRock’s IBIT ETF alone pulled in $2.63B inflows in a single week, pushing its total historic inflow to more than $65 billion. On another hand, Ethereum spot ETFs were approved and launched in May of 2024 and have reached a cumulative total net inflow of over $14.7 billion across all available ETFs.

These ETFs act as powerful on-ramps, channeling traditional capital into crypto in a regulated and familiar vehicle, which lowers friction for institutions and bridges traditional portfolios to BTC/ETH exposure.

With fewer barriers to entry, DATs can lean on these flows as validation. They don’t just signal demand, they help convert institutional capital into digital-asset treasuries that hold BTC/ETH as core reserves.

Favorable Regulatory Landscape

2025 has set an exceptionally favorable regulatory environment for cryptocurrencies, with both the SEC and the CFTC aligning on digital asset-related mandates. This coordination has created the most supportive regulatory landscape the industry has seen until now.

The GENIUS Act, passed in August 2025, established a formal framework for payment stablecoins, significantly reducing uncertainty around digital asset usage in the U.S. This has provided institutional players with greater clarity on compliance and has technically, paved the way for stablecoin adoption within treasuries.

Meanwhile, the CFTC’s Crypto Sprint Program has opened the door for spot crypto trading on federally registered futures exchanges, which effectively extends the regulatory oversight to a greater market segment. This has given more legitimacy and structure to spot trading, which has been a gap that previously hindered traditional finance participants to take part in it.

On another hand, the SEC has enabled staking for some ETFs after deciding earlier in 2025 that blockchain staking activities do not violate securities laws. Adding more to the momentum, in October of 2025, the SEC also approved the generic listing standards for commodity-based exchange-traded products, which could end up allowing new crypto funds to be fast-tracked by removing the requirements for individual ETF approvals. As a result, this could become yet another catalyst for continuous growth since more companies could offer ETFs more seamlessly, and in effect make crypto more accessible to retail users.

Together, these developments have set a favorable foundation for digital asset treasuries. With clearer compliance paths, a potential swarm of new ETF launches, inflows consistently reaching new highs, and rising institutional adoption, 2025 stands out as the year when holding digital assets shifted from speculation to a mainstream institutional strategy.

Interest Rates

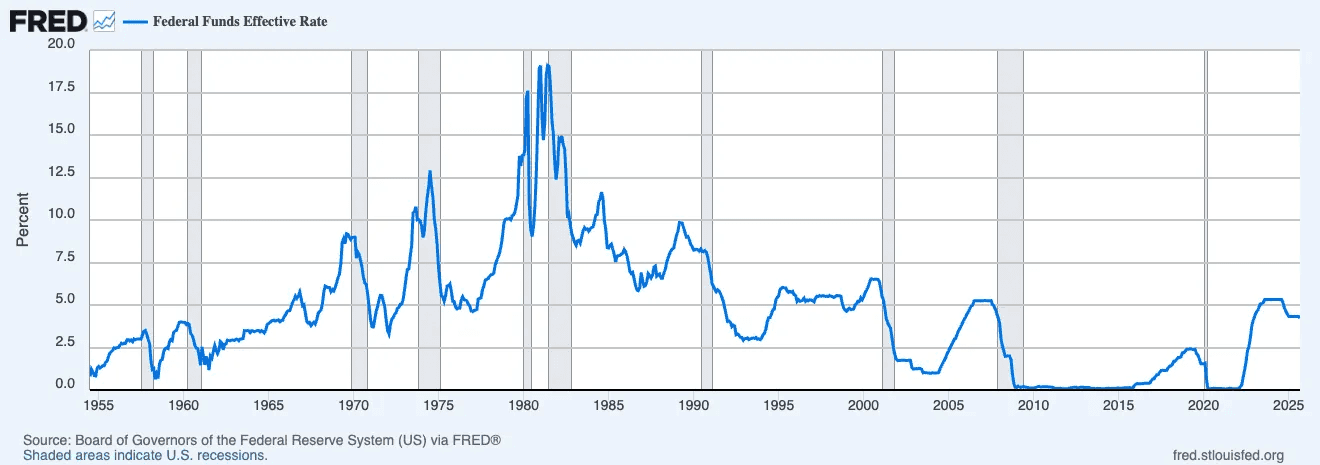

Although interest rates have been rising since 2022, they are still far below historic highs and peaks from the early 1980s. The more relevant contrast, however, is with the 2010s and the post-COVID near-zero scenario, today’s ~5% rates have made cash and short-term Treasuries attractive again.

Higher rates, however, have mainly benefitted stablecoin issuers. With reserves held in T-bills and repo, the issuers capture the yield while most holders earn nothing. Tether, for example, has generated billions in profit from its reserve income alone, effectively turning interest rates into a major revenue driver for stablecoins.

Nevertheless, DATs seem to be in the play for long-term appreciation and scarcity. While current rates are favorable for treasuries that hold cash, T-Bills, or even stablecoins, that safe yield will disappear in low or zero-rate scenarios (or even if real rates turn negative). As a result, treasuries are shifting towards adoption of BTC, ETH, and even SOL, as the core asset for long-term appreciation, doubling as a monetary-debasement hedge, and on-chain utility such as ETH staking yield and collateralized borrowing, among others.

Compounding Treasury Growth

Another driver behind the rise of DATs is one of their core selling points: the ability to grow net asset value (NAV) per share over time. Unlike ETFs or spot holdings that passively track token prices, DATs can actively expand their underlying asset base through strategic financing, treasury management, or yield-generating activities such as staking and lending. This means shareholders aren’t just exposed to price appreciation, but they can also benefit from an increasing share of underlying crypto ownership as the treasury grows.

In essence, owning a DAT can offer higher return potential than holding tokens directly or through an ETF, as investors capture both the market upside and the compounding effects of treasury expansion.

DeFi Integration

The integration of staking and DeFi strategies has become another growth catalyst for DATs, mainly those holding proof-of-stake assets like ETH or SOL. By staking their assets directly or through liquid staking derivatives (such as stETH or mSOL), DATs are able to generate on-chain yield while maintaining liquidity, turning once-idle reserves into productive capital.

Beyond staking, there are more DeFi integrations that allow DATs to leverage their assets such as using them in collateralized borrowing, liquidity provisioning, or restaking, adding flexibility and new revenue streams.

A Timeline of DAT Growth

The initial move by MicroStrategy, initially a business intelligence firm that on August 11 of 2020 announced the investment of $250 million into Bitcoin as part of a long-term investment strategy, provided a blueprint for other public companies to invest mainly in BTC, seeing it as an attractive investment asset and store of value with long-term appreciation and inflation hedging potential rather than holding cash.

How Digital Asset Treasuries Are Financed

The crypto assets held by DATs are largely purchased with capital that is raised via traditional instruments such as equity, debt, convertible notes, and private placements. These companies are effectively bridging conventional capital markets with crypto, raising funds through stock offerings, zero-interest bonds, SPACs, or PIPE deals, and then reallocating that capital into digital assets like Bitcoin or derivatives, or even collateralized loans to generate yield and expand their crypto holdings beyond simple accumulation.

Company / Treasury | Ticker | Financing Mechanisms |

|---|---|---|

MicroStrategy | MSTR | - Proceeds from equity and debt financings |

Bitmine Immersion Technologies | BMNR | - Raising capital from investors and leveraging stock market liquidity |

Bit Digital Inc. | BTBT | - Convertible notes offerings |

Sharplink Gaming Inc. | SBET | - Issuing shares to investors |

Nakamoto Holdings | NAKA | - Issuing equity at a premium to NAV and recycling proceeds to purchase BTC |

Metaplanet | MTPLF | - Zero-interest bonds for BTC purchases |

Upexi Inc. | UPXI | - Convertible notes backed by SOL |

DeFi Development Corp. | DFDV | - Equity placements, convertible structures, and debt financings |

Dynamix Corporation | ETHM | - Special Purpose Acquisition Company (SPAC) |

Ethzilla Corp. | ETHZ | - Capital raised via convertible debentures (convertible bonds) |

Forward Industries | FORD | - Private Investment in Public Equity (PIPE) financing |

Solana Company | HSDT | - PIPE offering |

Cantor Equity Partners | CEPO | - SPACs backed by major investors and institutions |

Bitcoin Standard Treasury Company | BSTR | - PIPE financing (common equity, convertible notes, preferred stock, BTC contributions) |

Sharps Technology | STSS | - Equity capital raised through private placement offering |

Quantifying Strength of Leading DATs: Holdings, Ratios, and Performance

To make sense of the growing DAT landscape, we can utilize three core ratios to assess how these companies may be priced relative to their crypto exposure. Together, these ratios give us a quick but powerful lens into how the market values digital asset treasuries not just for what they hold, but for how they operate.

The Crypto to Market Cap Ratio (CMCR) shows how much of a company’s market value is backed by its crypto holdings. A CMCR below 1 means the company trades at a premium, investors are valuing its strategy, management, or potential beyond the assets themselves. A CMCR above 1 signals a discount, suggesting the market values the equity at less than the worth of its crypto.

The NAV Premium or Discount expresses that same relationship as a percentage calculated by dividing the difference between market cap and holdings value by the holdings value. A positive ratio indicates a premium whereas a negative one marks a discount. This figure helps show where investor sentiment lies: premiums for companies perceived as strong operators, discounts where the market questions management, liquidity, or reporting clarity.

Crypto per Share (CPS) measures direct exposure by showing how much crypto or crypto value backs each share. It’s an easy way for investors to have a sense of how much BTC, ETH, or SOL they’re effectively buying when they purchase a share.

Name | Ticker | Asset Held | Quantity | Crypto Holdings Value | Market Cap | # of Shares | Crypto to Market Cap Ratio | NAV Premium / Discount | Crypto per Share (USD) | Crypto per Share (Asset) |

|---|---|---|---|---|---|---|---|---|---|---|

Microstrategy | MSTR | BTC | 640,418 | $69,501,363,450 | $85,221,000,000.00 | 267,470,000 | 0.82 | 0.23 | $260 | 0.00239 |

Bitmine Immersion Technologies Inc | BMNR | ETH | 3,240,000 | $12,519,036,000 | $15,052,399,818.00 | 173,500,000 | 0.83 | 0.20 | $72 | 0.01867 |

Twenty One | CEP | BTC | 43,514 | $4,722,855,085 | $201,983,000 | 346,470,000 | 23.38 | -0.96 | $14 | 0.00013 |

Metaplanet | MTPLF | BTC | 30,823 | $3,341,166,349 | $4,274,490,944.00 | 1,140,000,000 | 0.78 | 0.28 | $3 | 0.00003 |

Sharplink Gaming Inc | SBET | ETH | 859,853 | $3,322,386,006 | $2,817,902,355.00 | 196,690,000 | 1.18 | -0.15 | $17 | 0.00437 |

Bitcoin Standard Treasury Company/Cantor Equity Partners | CEPO | BTC | 30,021 | $3,252,112,786 | $268,510,000 | 20,500,000 | 12.11 | -0.92 | $159 | 0.00146 |

Dynamix Corp (The Ether Machine) | ETHM | ETH | 495,362 | $1,906,455,146 | $273,901,169.00 | 16,600,000 | 6.96 | -0.86 | $115 | 0.02984 |

Forward Industries | FORD | SOL | 6,822,000 | $1,264,457,700 | $2,062,890,804.00 | 86,020,000 | 0.61 | 0.63 | $15 | 0.07931 |

Nakamoto Holdings | NAKA | BTC | 5,765 | $623,938,109 | $297,059,350.00 | 413,600,000 | 2.10 | -0.52 | $2 | 0.00001 |

Bit Digital Inc | BTBT | ETH | 150,244 | $580,464,689 | $1,272,873,583.00 | 321,430,000 | 0.46 | 1.19 | $2 | 0.00047 |

Solana Company | HSDT | SOL | 2,200,000 | $407,946,000 | $1,179,641,330.00 | 40,300,000 | 0.35 | 1.89 | $10 | 0.05459 |

DeFi Development Corp | DFDV | SOL | 2,195,926 | $407,190,558 | $384,281,517.00 | 28,890,000 | 1.06 | -0.06 | $14 | 0.07601 |

Ethzilla Corp | ETHZ | ETH | 102,246 | $394,062,218 | $273,901,169.00 | 16,020,000 | 1.44 | -0.30 | $25 | 0.00638 |

Upexi Inc | UPXI | SOL | 2,018,419 | $374,275,435 | $361,310,156.00 | 58,890,000 | 1.04 | -0.03 | $6 | 0.03427 |

Sharps Technology | STSS | SOL | 2,000,000 | $370,500,000 | $366,664,878.00 | 26,600,000 | 1.01 | -0.01 | $14 | 0.07519 |

While the companies above have digital asset accumulation at the core of their strategy, several other public companies also hold significant amounts of crypto on their balance sheets and in some cases, they even surpass the totals of the crypto-focused treasuries. These firms have varied business models, ranging from mining and exchange operations to media and technology.

The top five among them include Marathon Digital Holdings (MARA), one of the largest publicly traded Bitcoin miners in the U.S., Hut 8, a major Canadian mining company, Bullish, the US-based exchange, Riot Platforms, another prominent American Bitcoin miner, and Trump Media & Technology Group, the media company majorly owned by President Donald Trump.

Despite differing core businesses, these five stand out as the largest non-DAT public holders of crypto, but they’re only a few from a long list. Dozens of other listed companies across industries report some form of digital asset exposure. They highlight that digital assets are no longer reserved for specialized treasuries, but they are also becoming a staple on balance sheets across the broader corporate landscape, signaling a deeper institutional acceptance of crypto as a strategic reserve asset.

Name | Ticker | Asset Held | Quantity | Crypto Holdings Value | Market Cap | # of Shares |

|---|---|---|---|---|---|---|

MARA Holdings | MARA | BTC | 53,250 | $5,772,219,060 | $7,435,000,000 | 370,460,000 |

Hut 8 Mining Corp | HUT | BTC | 10,667 | $1,158,233,847 | $4,951,000,000 | 105,530,000 |

Bullish | BLSH | BTC | 24,300 | $2,637,435,735 | $8,372,000,000 | 146,180,000 |

Riot Platforms | RIOT | BTC | 19,287 | $2,094,070,595 | $7,640,000,000 | 369,620,000 |

Trump Media & Technology Group Corp. | DJT | BTC | 15,000 | $1,628,613,000 | $4,520,000,000 | 279,870,000 |

What are DATs?

Digital Asset Treasuries (DATs) are publicly traded companies that make on-chain assets (such as BTC, ETH, SOL) a core part of their balance sheet and strategy, giving investors equity exposure to those assets plus whatever operating leverage and additional benefits the team can add.

In practice, DATs raise capital via equity offerings, convertible notes, or debt, and deploying it into crypto. Many of them can or have plans to further expand the treasury’s utility by putting it to work by staking PoS assets, using liquid staking tokens, lending, or collateralized borrowing to generate yield and grow holdings. Unlike ETFs, DATs can time purchases, use financing, and actively manage exposure, which can expand Net Asset Value (NAV) per share over time.

For investors, returns can come from three places: the underlying token appreciation, treasury growth per share (via accumulation and yield), and the equity premium/discount the market assigns to the share. This mix is what differentiates DATs from simply holding crypto or buying an ETF.

What’s Driving the Rise of DATs Today?

With the appearance of dozens of Digital Asset Treasuries (DATs), it’s clear that this is a new class of vehicle for retail to enter crypto, and it is well different from traditional treasuries built around cash and bonds. The model isn’t at an experiment-stage anymore either: early movers like MicroStrategy have already proved the model with large, sustained BTC accumulation, and a newer wave is expanding beyond Bitcoin into ETH and SOL, effectively treating crypto assets as core balance sheet reserves rather than merely risky bets.

What sets DATs apart is that they’re not just passive wrappers. They can raise capital (equity, debt, etc.), deploy it into crypto, and then work those reserves through staking, lending, collateralized borrowing, or even restaking, to grow holdings and NAV per share over time. That means shareholders can capture both market appreciation and treasury expansion, which are benefits that users don’t get from holding ETFs, for example.

So why are DATs going all-in now? A mix of factors: ETFs as on-ramps bringing regulated capital into BTC/ETH, a more favorable regulatory landscape, a favorable rate scenario that’s changing how investors view cash vs. scarcity assets, compounding treasury growth potential that accrues NAV per share, and the possibility for deeper DeFi integration that can turn static reserve balances into productive capital. Let’s break down each factor.

ETFs as On-Ramps

Since the approval of spot BTC ETFs back in 2024, demand has been staggering: daily trading volume surpasses $7B, and BlackRock’s IBIT ETF alone pulled in $2.63B inflows in a single week, pushing its total historic inflow to more than $65 billion. On another hand, Ethereum spot ETFs were approved and launched in May of 2024 and have reached a cumulative total net inflow of over $14.7 billion across all available ETFs.

These ETFs act as powerful on-ramps, channeling traditional capital into crypto in a regulated and familiar vehicle, which lowers friction for institutions and bridges traditional portfolios to BTC/ETH exposure.

With fewer barriers to entry, DATs can lean on these flows as validation. They don’t just signal demand, they help convert institutional capital into digital-asset treasuries that hold BTC/ETH as core reserves.

Favorable Regulatory Landscape

2025 has set an exceptionally favorable regulatory environment for cryptocurrencies, with both the SEC and the CFTC aligning on digital asset-related mandates. This coordination has created the most supportive regulatory landscape the industry has seen until now.

The GENIUS Act, passed in August 2025, established a formal framework for payment stablecoins, significantly reducing uncertainty around digital asset usage in the U.S. This has provided institutional players with greater clarity on compliance and has technically, paved the way for stablecoin adoption within treasuries.

Meanwhile, the CFTC’s Crypto Sprint Program has opened the door for spot crypto trading on federally registered futures exchanges, which effectively extends the regulatory oversight to a greater market segment. This has given more legitimacy and structure to spot trading, which has been a gap that previously hindered traditional finance participants to take part in it.

On another hand, the SEC has enabled staking for some ETFs after deciding earlier in 2025 that blockchain staking activities do not violate securities laws. Adding more to the momentum, in October of 2025, the SEC also approved the generic listing standards for commodity-based exchange-traded products, which could end up allowing new crypto funds to be fast-tracked by removing the requirements for individual ETF approvals. As a result, this could become yet another catalyst for continuous growth since more companies could offer ETFs more seamlessly, and in effect make crypto more accessible to retail users.

Together, these developments have set a favorable foundation for digital asset treasuries. With clearer compliance paths, a potential swarm of new ETF launches, inflows consistently reaching new highs, and rising institutional adoption, 2025 stands out as the year when holding digital assets shifted from speculation to a mainstream institutional strategy.

Interest Rates

Although interest rates have been rising since 2022, they are still far below historic highs and peaks from the early 1980s. The more relevant contrast, however, is with the 2010s and the post-COVID near-zero scenario, today’s ~5% rates have made cash and short-term Treasuries attractive again.

Higher rates, however, have mainly benefitted stablecoin issuers. With reserves held in T-bills and repo, the issuers capture the yield while most holders earn nothing. Tether, for example, has generated billions in profit from its reserve income alone, effectively turning interest rates into a major revenue driver for stablecoins.

Nevertheless, DATs seem to be in the play for long-term appreciation and scarcity. While current rates are favorable for treasuries that hold cash, T-Bills, or even stablecoins, that safe yield will disappear in low or zero-rate scenarios (or even if real rates turn negative). As a result, treasuries are shifting towards adoption of BTC, ETH, and even SOL, as the core asset for long-term appreciation, doubling as a monetary-debasement hedge, and on-chain utility such as ETH staking yield and collateralized borrowing, among others.

Compounding Treasury Growth

Another driver behind the rise of DATs is one of their core selling points: the ability to grow net asset value (NAV) per share over time. Unlike ETFs or spot holdings that passively track token prices, DATs can actively expand their underlying asset base through strategic financing, treasury management, or yield-generating activities such as staking and lending. This means shareholders aren’t just exposed to price appreciation, but they can also benefit from an increasing share of underlying crypto ownership as the treasury grows.

In essence, owning a DAT can offer higher return potential than holding tokens directly or through an ETF, as investors capture both the market upside and the compounding effects of treasury expansion.

DeFi Integration

The integration of staking and DeFi strategies has become another growth catalyst for DATs, mainly those holding proof-of-stake assets like ETH or SOL. By staking their assets directly or through liquid staking derivatives (such as stETH or mSOL), DATs are able to generate on-chain yield while maintaining liquidity, turning once-idle reserves into productive capital.

Beyond staking, there are more DeFi integrations that allow DATs to leverage their assets such as using them in collateralized borrowing, liquidity provisioning, or restaking, adding flexibility and new revenue streams.

A Timeline of DAT Growth

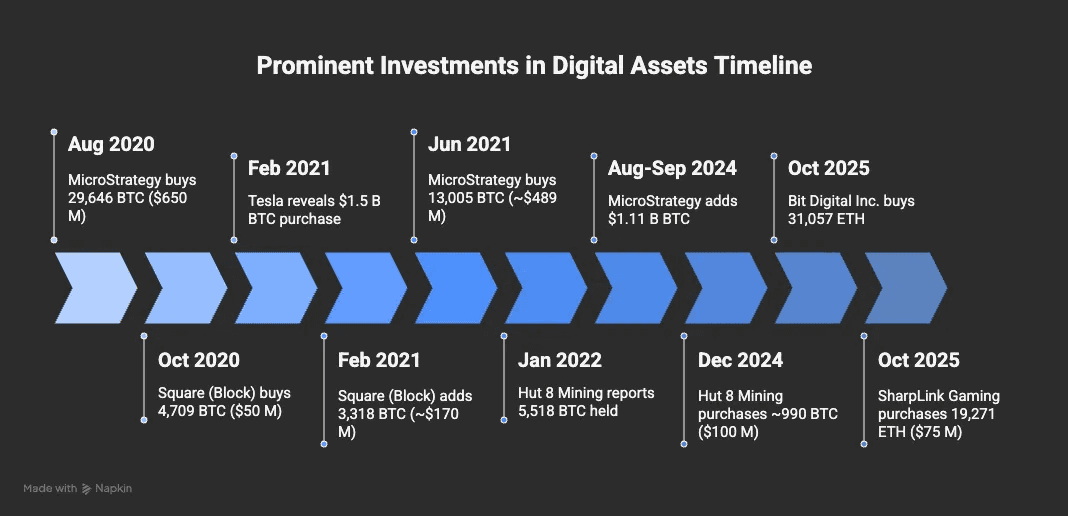

The initial move by MicroStrategy, initially a business intelligence firm that on August 11 of 2020 announced the investment of $250 million into Bitcoin as part of a long-term investment strategy, provided a blueprint for other public companies to invest mainly in BTC, seeing it as an attractive investment asset and store of value with long-term appreciation and inflation hedging potential rather than holding cash.

How Digital Asset Treasuries Are Financed

The crypto assets held by DATs are largely purchased with capital that is raised via traditional instruments such as equity, debt, convertible notes, and private placements. These companies are effectively bridging conventional capital markets with crypto, raising funds through stock offerings, zero-interest bonds, SPACs, or PIPE deals, and then reallocating that capital into digital assets like Bitcoin or derivatives, or even collateralized loans to generate yield and expand their crypto holdings beyond simple accumulation.

Company / Treasury | Ticker | Financing Mechanisms |

|---|---|---|

MicroStrategy | MSTR | - Proceeds from equity and debt financings |

Bitmine Immersion Technologies | BMNR | - Raising capital from investors and leveraging stock market liquidity |

Bit Digital Inc. | BTBT | - Convertible notes offerings |

Sharplink Gaming Inc. | SBET | - Issuing shares to investors |

Nakamoto Holdings | NAKA | - Issuing equity at a premium to NAV and recycling proceeds to purchase BTC |

Metaplanet | MTPLF | - Zero-interest bonds for BTC purchases |

Upexi Inc. | UPXI | - Convertible notes backed by SOL |

DeFi Development Corp. | DFDV | - Equity placements, convertible structures, and debt financings |

Dynamix Corporation | ETHM | - Special Purpose Acquisition Company (SPAC) |

Ethzilla Corp. | ETHZ | - Capital raised via convertible debentures (convertible bonds) |

Forward Industries | FORD | - Private Investment in Public Equity (PIPE) financing |

Solana Company | HSDT | - PIPE offering |

Cantor Equity Partners | CEPO | - SPACs backed by major investors and institutions |

Bitcoin Standard Treasury Company | BSTR | - PIPE financing (common equity, convertible notes, preferred stock, BTC contributions) |

Sharps Technology | STSS | - Equity capital raised through private placement offering |

Quantifying Strength of Leading DATs: Holdings, Ratios, and Performance

To make sense of the growing DAT landscape, we can utilize three core ratios to assess how these companies may be priced relative to their crypto exposure. Together, these ratios give us a quick but powerful lens into how the market values digital asset treasuries not just for what they hold, but for how they operate.

The Crypto to Market Cap Ratio (CMCR) shows how much of a company’s market value is backed by its crypto holdings. A CMCR below 1 means the company trades at a premium, investors are valuing its strategy, management, or potential beyond the assets themselves. A CMCR above 1 signals a discount, suggesting the market values the equity at less than the worth of its crypto.

The NAV Premium or Discount expresses that same relationship as a percentage calculated by dividing the difference between market cap and holdings value by the holdings value. A positive ratio indicates a premium whereas a negative one marks a discount. This figure helps show where investor sentiment lies: premiums for companies perceived as strong operators, discounts where the market questions management, liquidity, or reporting clarity.

Crypto per Share (CPS) measures direct exposure by showing how much crypto or crypto value backs each share. It’s an easy way for investors to have a sense of how much BTC, ETH, or SOL they’re effectively buying when they purchase a share.

Name | Ticker | Asset Held | Quantity | Crypto Holdings Value | Market Cap | # of Shares | Crypto to Market Cap Ratio | NAV Premium / Discount | Crypto per Share (USD) | Crypto per Share (Asset) |

|---|---|---|---|---|---|---|---|---|---|---|

Microstrategy | MSTR | BTC | 640,418 | $69,501,363,450 | $85,221,000,000.00 | 267,470,000 | 0.82 | 0.23 | $260 | 0.00239 |

Bitmine Immersion Technologies Inc | BMNR | ETH | 3,240,000 | $12,519,036,000 | $15,052,399,818.00 | 173,500,000 | 0.83 | 0.20 | $72 | 0.01867 |

Twenty One | CEP | BTC | 43,514 | $4,722,855,085 | $201,983,000 | 346,470,000 | 23.38 | -0.96 | $14 | 0.00013 |

Metaplanet | MTPLF | BTC | 30,823 | $3,341,166,349 | $4,274,490,944.00 | 1,140,000,000 | 0.78 | 0.28 | $3 | 0.00003 |

Sharplink Gaming Inc | SBET | ETH | 859,853 | $3,322,386,006 | $2,817,902,355.00 | 196,690,000 | 1.18 | -0.15 | $17 | 0.00437 |

Bitcoin Standard Treasury Company/Cantor Equity Partners | CEPO | BTC | 30,021 | $3,252,112,786 | $268,510,000 | 20,500,000 | 12.11 | -0.92 | $159 | 0.00146 |

Dynamix Corp (The Ether Machine) | ETHM | ETH | 495,362 | $1,906,455,146 | $273,901,169.00 | 16,600,000 | 6.96 | -0.86 | $115 | 0.02984 |

Forward Industries | FORD | SOL | 6,822,000 | $1,264,457,700 | $2,062,890,804.00 | 86,020,000 | 0.61 | 0.63 | $15 | 0.07931 |

Nakamoto Holdings | NAKA | BTC | 5,765 | $623,938,109 | $297,059,350.00 | 413,600,000 | 2.10 | -0.52 | $2 | 0.00001 |

Bit Digital Inc | BTBT | ETH | 150,244 | $580,464,689 | $1,272,873,583.00 | 321,430,000 | 0.46 | 1.19 | $2 | 0.00047 |

Solana Company | HSDT | SOL | 2,200,000 | $407,946,000 | $1,179,641,330.00 | 40,300,000 | 0.35 | 1.89 | $10 | 0.05459 |

DeFi Development Corp | DFDV | SOL | 2,195,926 | $407,190,558 | $384,281,517.00 | 28,890,000 | 1.06 | -0.06 | $14 | 0.07601 |

Ethzilla Corp | ETHZ | ETH | 102,246 | $394,062,218 | $273,901,169.00 | 16,020,000 | 1.44 | -0.30 | $25 | 0.00638 |

Upexi Inc | UPXI | SOL | 2,018,419 | $374,275,435 | $361,310,156.00 | 58,890,000 | 1.04 | -0.03 | $6 | 0.03427 |

Sharps Technology | STSS | SOL | 2,000,000 | $370,500,000 | $366,664,878.00 | 26,600,000 | 1.01 | -0.01 | $14 | 0.07519 |

While the companies above have digital asset accumulation at the core of their strategy, several other public companies also hold significant amounts of crypto on their balance sheets and in some cases, they even surpass the totals of the crypto-focused treasuries. These firms have varied business models, ranging from mining and exchange operations to media and technology.

The top five among them include Marathon Digital Holdings (MARA), one of the largest publicly traded Bitcoin miners in the U.S., Hut 8, a major Canadian mining company, Bullish, the US-based exchange, Riot Platforms, another prominent American Bitcoin miner, and Trump Media & Technology Group, the media company majorly owned by President Donald Trump.

Despite differing core businesses, these five stand out as the largest non-DAT public holders of crypto, but they’re only a few from a long list. Dozens of other listed companies across industries report some form of digital asset exposure. They highlight that digital assets are no longer reserved for specialized treasuries, but they are also becoming a staple on balance sheets across the broader corporate landscape, signaling a deeper institutional acceptance of crypto as a strategic reserve asset.

Name | Ticker | Asset Held | Quantity | Crypto Holdings Value | Market Cap | # of Shares |

|---|---|---|---|---|---|---|

MARA Holdings | MARA | BTC | 53,250 | $5,772,219,060 | $7,435,000,000 | 370,460,000 |

Hut 8 Mining Corp | HUT | BTC | 10,667 | $1,158,233,847 | $4,951,000,000 | 105,530,000 |

Bullish | BLSH | BTC | 24,300 | $2,637,435,735 | $8,372,000,000 | 146,180,000 |

Riot Platforms | RIOT | BTC | 19,287 | $2,094,070,595 | $7,640,000,000 | 369,620,000 |

Trump Media & Technology Group Corp. | DJT | BTC | 15,000 | $1,628,613,000 | $4,520,000,000 | 279,870,000 |

Simplicity Consultancy FZ LTD

Social

Simplicity Consultancy FZ LTD

Social

Simplicity Consultancy FZ LTD

Social